The Economics Hub Newsletter: Week 5

Euro-dollar parity, ECB's policy dilemma, US inflation, rising global military spending, crypto regulations, podcasts and other article recommendations

Happy Saturday!

Welcome to another issue of The Economics Hub Newsletter! I hope you are well.

If you have already subscribed, thank you! If you are here for the first time, then please consider subscribing for free educational content and resources!

Here’s what we cover this week. As per your interest and convenience, please click on the specific topic to jump directly to that section!

Ready? Let’s dive in!

The European Central Bank’s policy dilemma amidst rising inflation and broadening bond spreads

RBI allows payments for cross-border trade in rupee, move to benefit trade with Russia

Global Financial Watchdog FSB to Propose Crypto Regulations in October

Podcast Recommendations of the Week

1. Euro hits US dollar parity for the first time in 20 years

Since the start of the Russo-Ukrainian war, there have been major incidences of currencies having a sharp decline against the mighty dollar, and the unlucky winner for July is the euro. The eurozone currency, shared by Germany, France, Italy and 16 others, is flirting with parity to the U.S. dollar for the first time since 2002.

Euro has depreciated by almost 12% against the dollar since the start of the year when one euro bought about $1.14. This may seem like no big deal unless you’re a currency trader or policymaker. However, such currency declines are unusual in developed economies. But sharp movements in exchange rates create uncertainty and can lead to economic and financial instability.

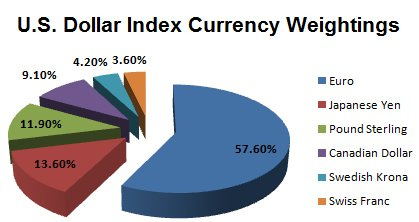

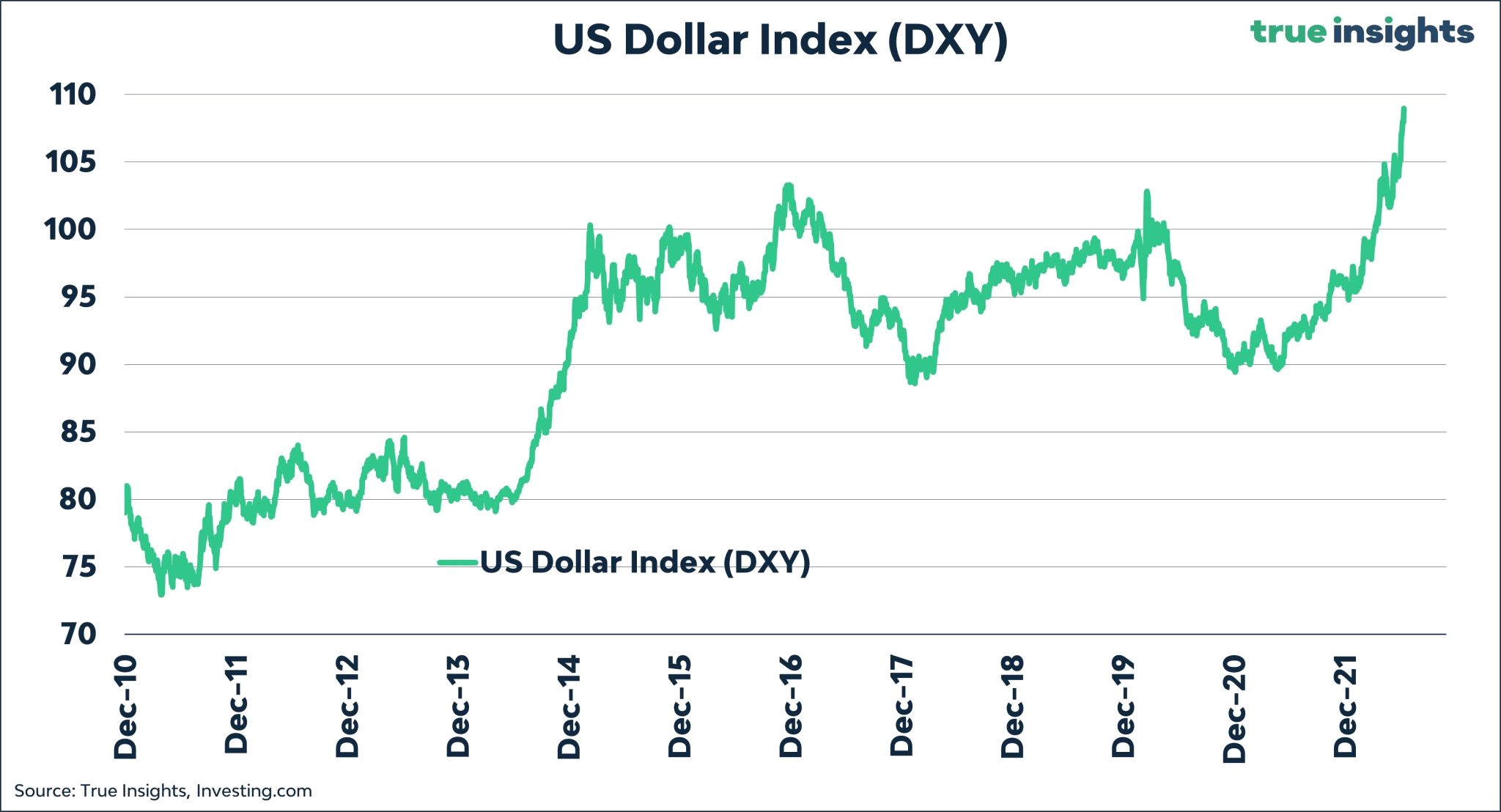

The decline in the Euro has also been crucial in strengthening the US dollar Index - a measure of the value of the U.S. dollar relative to a basket of foreign currencies, as the euro is the largest component of the index, making up 57.6% of the basket.

What caused the sharp decline in EURUSD? There are several factors, and they include:

Monetary policy: the U.S. Federal Reserve (Fed) has been tightening policy much more aggressively than the European Central Bank (ECB).

Trade balances: While both the U.S. and Europe have seen a deterioration in their trade balances, the eurozone has seen an especially sharp decline in its trade surplus in recent months as European natural gas prices soared.

Geopolitical reasons: The war in Ukraine has created geopolitical uncertainty and is driving up energy prices, especially in Europe given their vulnerability and high dependence on Russian energy supplies. Monday’s shutdown of the Nord Stream 1 natural-gas pipeline into Germany, apparently for maintenance, contributed to the latest pressure on the euro.

Intra-European bond spreads: Increasing tension within the eurozone debt market also appears to be weighing on the euro. In layman’s terms, there has been a sharp increase in yields in nations with higher levels of public debt such as Italy. Wider sovereign spreads between Germany and nations like Italy appear to be weighing on the euro. Instead of fighting inflation, the ECB is focused on extending monetary ease to these nations with high public debt to prevent “fragmentation.”

All these factors are weighing on the euro amidst issues of the European Central bank’s credibility. As Nobel economist Robert Mundell once observed, the dollar-euro exchange rate is the most important in the world, “and neither Europe nor the United States is going to want to have big fluctuations in that price.” This statement holds so much significance in today’s world of economic and geopolitical uncertainty.

2. The European Central Bank is Trapped. Here’s Why.

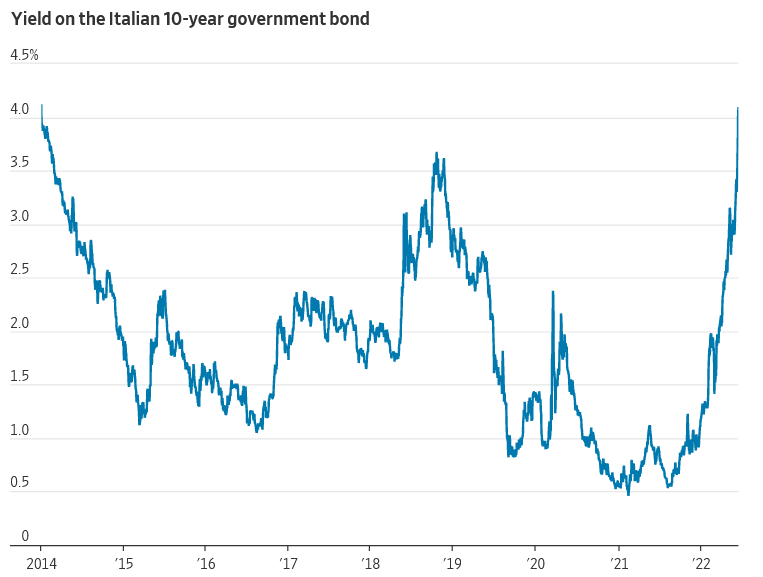

We just discussed the widening bond spreads between European countries and how it is weighing on the euro. But what exactly is the European bond spread? How did we get here? What policy options does the European Central Bank have to mitigate the imminent fragmentation risk? Well, to begin with, the European bond spreads are essentially concerned with the spread between highly rated German bonds and bonds of countries with high government debt such as Italy, Greece, etc. If you are unfamiliar with bond yield, it simply means the returns that an investor obtains from a bond.

As you can see from the chart, the yield on Italian government bonds has risen to an all-time high since 2014. This has been happening as investors continue to dump the bonds of the eurozone's most vulnerable members (including Italy) due to their uncertain economic outlook and their potential inability to service debt due to their high debt levels.

Consequently, markets have become increasingly concerned about ‘fragmentation risk’ in the euro area. Now, the European Central Bank has committed to mitigating “fragmentation risk” and pledged to "accelerate the completion of the design of a new anti-fragmentation instrument".

The details of their anti-fragmentation tool remain unclear. Experience from the past has shown that only asset purchases are (relatively) effective in controlling bond spreads. But this is where the trouble begins and ECB’s policy dilemma arises. In usual times, the ECB would have temporarily managed to keep the bond yields of peripheral countries in check via lower interest rates or asset purchase programs. But we are in a different time frame now with altogether different economic challenges. Amidst rising inflation due to multiple factors, the ECB is now also compelled to hike interest rates.

The interest rate hikes and the rollback of quantitative easing will add pressure to the “fragmentation risk.” With the ECB no longer buying significant quantities of bonds, demand will fall, which will depress prices further and increase yields. In the end, it is unclear how the ECB would address this policy dilemma and to what extent they can assure the global investors about the credibility of their anti-fragmentation tool.

While this is the explanation of the present situation, the mentioned article by Lyn Alden dives deeper into the fundamental reasons why we got here. She asserts that much of the European debt’s problems stem from their common framework of “A Monetary Union Without a Fiscal Union.” The article is illuminating and thought-provoking, I cannot recommend it enough!

3. Sri Lanka’s Road to Ruin Was Political, Not Economic

This article was recently shared by one of my friends whose opinions I truly admire and respect. It gave me an alternative perspective to think about the ongoing Sri Lankan crisis. As most of the readers of this blog are from the finance field, it is quite a possibility that we are not aware of this line of thinking which is not characteristic of the finance profession. Therefore, I am sharing it with you so that you can have an alternative perspective while navigating the Sri Lankan political and economic crisis.

The article does not overlook or refute the economic factors such as high external debt, reliance on the tourism industry, fertilizer ban that intensified the food crisis, depleting forex reserves and debt defaults that have affected the country’s credit quality but rather compel us to consider the deeper problems of Sri Lankan society that have always persisted and led to the current dire socio-economic and political situation. As the author brilliantly puts it:

The proximate cause of the protests is ruinous economic policies, but what put the Rajapaksa family in power—a family formerly considered village bumpkins—was Sinhalese Buddhist nationalism. It was nationalism that enabled governance rooted in meritocracy to be supplanted by ethnocracy, which over time has led to kakistocracy— governance by a country’s worst citizens.

So essentially, the author points out the two major factors that have enabled the government to pursue corrupt policies without any accountability at the expense of people’s livelihood. These factors are:

Sinhalese Buddhist nationalism: The Sinhalese, currently 75 percent of the population, subscribe to an ideology that claims they are the island’s original settlers and that all others—including Tamils (around 15 percent) and Muslims (around 10 percent)—live there thanks to majoritarian sufferance. Sri Lanka’s ethnocracy started when Prime Minister S.W.R.D. Bandaranaike made Sinhala the only official language in 1956 and successive governments thereby avoided hiring and promoting Tamils in particular.

Kleptocracy: The administrative services influenced by ethnocracy were likewise gutted over the same period, enabling cabinet ministers to lord over ministries that competent and professional cabinet secretaries previously managed. The government basically wanted ethnocentric administrative and law enforcement bodies. As the integrity of the democratic institutions was undermined, many competent and qualified individuals moved abroad over the years. This brain drain amid ethnocentric recruitment saw standards decline throughout government sectors and eventually led to us the current situation.

These are the two major factors that the author shed the light upon. You can read the entire article for a better understanding. The Caravan has also published an article on the same topic last month, please check that out as well if interested!

4. Trade transactions will soon be in rupee as RBI brings in a mechanism to hedge the currency

The Reserve Bank of India (RBI) has said that it is introducing a new mechanism this week for international trade settlements in rupees, aiming to promote exports and facilitate imports. While the move is seen to benefit trading primarily with Russia, it is also likely to help check dollar outflow and slow rupee depreciation to a “very limited extent”.

How will this system work?

For importers: To settle trade deals, authorised Indian banks will need to open Special Rupee Vostro Accounts of the partner trading country’s bank. Indian importers using this mechanism will need to pay in rupees. This will be credited into the special Vostro account of the correspondent bank of the partner country against the invoices for the supply of goods or services.

For exporters: Indian exporters, on the other hand, will be paid in rupees from the balance in the designated special Vostro account of the correspondent bank of the partner country.

So far in the currency markets and before Russia was cut off from the SWIFT system, if a company exports or imports, transactions were always in a foreign currency (excluding with countries like Nepal and Bhutan). So in the case of imports, the Indian company had to pay in a foreign currency (mainly dollars and could also include currencies like pounds, Euro, yen etc.). The Indian company gets paid in foreign currency in case of exports and the company converts that foreign currency to rupee since it needs rupee for its needs, in most cases.

Moreover, the move to facilitate trade settlement in rupees could also allow India to bypass certain orders that prevent the use of a global currency such as the US dollar for trade with certain countries. For instance, Russia’s attack on Ukraine has seen several countries impose sanctions on the former, with the US cutting off Russia’s access to the dollar. This has made Indian companies, looking to take advantage of the lower price of Russian commodities, consider alternative modes of payment for imports. I am not sure how this system would work in reality and its effect on the Indian rupee, but it is very important to watch the developments closely.

5. Global Military Spending Hits a Record High

In late April, new figures published by the Stockholm International Peace Research Institute (SIPRI) revealed that annual global military spending for 2021 had passed $2 trillion for the first time, reaching a staggering sum of $2.113 trillion. Last year was also the seventh straight year in which military spending around the world increased, with total expenditure almost doubling in this century alone. The five largest spenders in 2021 were the United States, China, India, the United Kingdom and Russia, together accounting for 62 per cent of expenditure.

The US, with just over 4 percent of the world’s population, accounts for nearly 40 percent of all global military spending. In an attempt to preserve a technological advantage over its competitors, US funding for military research and development has increased significantly, the report noted.

Russia increased its military expenditure by 2.9 per cent in 2021, to $65.9 billion, at a time when it was building up its forces along the Ukrainian border. ‘High oil and gas revenues helped Russia to boost its military spending in 2021. Russian military expenditure had been in decline between 2016 and 2019 as a result of low energy prices combined with sanctions in response to Russia’s annexation of Crimea in 2014,’ said Lucie Béraud-Sudreau, Director of SIPRI’s Military Expenditure and Arms Production Programme.

India’s military spending of $76.6 billion ranked third highest in the world. This was up by 0.9 per cent from 2020 and by 33 per cent from 2012. In a push to strengthen the indigenous arms industry, 64 per cent of capital outlays in the military budget of 2021 were earmarked for acquisitions of domestically produced arms.

China’s economic rise from a predominantly rural society in the 1970s to a motor of the world economy today has been accompanied by a rapid expansion of its military capabilities. Last year, the Chinese government allocated an estimated US$293 billion to its military. After increasing its spending for 27 consecutive years, it now accounts for 14 percent of global spending.

To summarize, the world continues to arm itself at an alarming rate, perhaps more fervently than ever before. And in 2022, despite all the global economic challenges we are facing, it does not appear to be slowing down in the coming years, given the geopolitical instability. It is not just the usual big spenders that are boosting their military capabilities. A growing number of countries with defence capabilities that, up until very recently, could only be described as limited have even joined in on the burgeoning arms race.

The article is informative but unfortunately, it does not highlight the terrorization of the world caused by US military forces and its allies, in the middle-east, Latin America and elsewhere over the last many decades. Maintaining the global superiority and status quo of the United States is at the heart of the Military Industrial Complex and is primarily responsible for committing major war crimes, conflicts, invasions, overthrowing governments for vested interests, etc. all around the world. Blaming China and Russia is easy but utterly overlooking the role, existence and influence of the Military Industrial Complex is a sheer disrespect to the lives of millions of people lost due to American-led or backed military operations.

6. Fueling the Warfare State

Read this brilliant article by William Hartung instead, which highlights the increased militarization efforts taken by the United States in Europe and Asia, in recent months. It is not just the increased militarization efforts but also increasingly budgetary allocation to the American national security state including military, intelligence, and internal-security expenditures. The author brilliantly puts it:

This lust for yet more weapons spending is especially misguided at a time when a never-ending pandemic, growing heat waves and other depredations of climate change, and racial and economic injustice are devastating the lives of millions of Americans. In a world where such dangers are only increasing, perhaps the best hope for launching a process that could, sooner or later, reverse such perverse priorities lies with grassroots organizing. Consider, for instance the “moral budget” crafted by the Poor People’s Campaign, which would cut Pentagon spending almost in half while refocusing on programs aimed at eliminating poverty, protecting the environment, and improving access to health care. If even part of such an agenda were achieved and the “defense” budget reined in, if not cut drastically, America and the world would be far safer places.

Please read the article by William Hartung and Poor People Campaign’s report for more details!

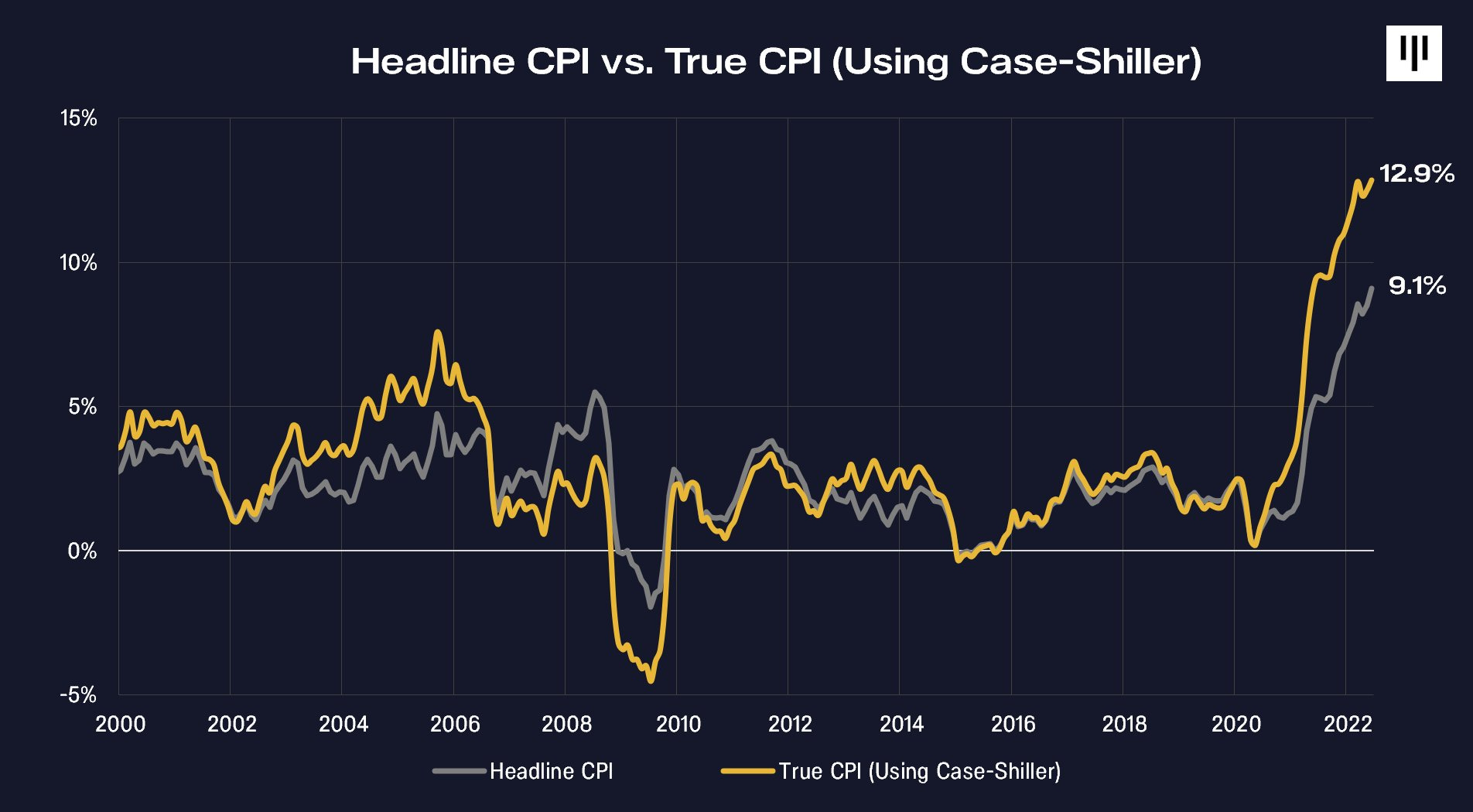

7. US inflation accelerates to 9.1%, the highest in 41 years

US inflation accelerated in June by more than forecast, underscoring relentless price pressures that will keep the Federal Reserve on track for another big interest-rate hike later this month. The consumer price index rose 9.1% from a year earlier, the largest gain since the end of 1981, Labor Department data showed Wednesday. The widely followed inflation gauge increased 1.3% from a month earlier, the most since 2005, reflecting higher gasoline, shelter and food costs.

The so-called core CPI, which strips out the more volatile food and energy components, advanced 0.7% from the prior month and 5.9% from a year ago, all figures are exceeding analysts' forecasts and piling further pressure on the Federal Reserve to bring it down with faster interest rate rises.

Dan Morehead, CEO of Pantera Capital makes an assertive comment that the actual inflation figures are way above the official figures. He uses the Case-Shiller Index, an alternative real-time measurement for housing inflation in place of OER (owners' equivalent rent) – a very slow-moving index introduced in 1982.

If you were to ask me, the *actual* inflation figures are possibly way higher than that and honestly, it differs from person to person living in different regions with their respective consumption pattern on a specific basket of goods and services. I mean, as we buy goods and services and observe their prices, we get a sense of how fast prices change. But quite often our perceptions do not match the official inflation figures. This is primarily because a person’s monthly/yearly basket of goods and services does not coincide with the basket of goods and services that the government uses to measure inflation. In a current macro-framework, a person who spends disproportionately higher on food, fuel and housing rent might be experiencing a way harsher inflation.

8. The Costs of Using Buy Now, Pay Later (BNPL) Products

A couple of weeks back we discussed the potential dangers of using BNPL products and why you should be mindful while opting for such credit-based products. Buy Now Pay Later (BNPL) schemes let consumers finance payments for items such as clothes and furniture on credit with no interest or charges – unless they fail to pay back on time, at which point many firms impose late fees. In a short period, these products have become one of the popular modes for customers to make retail purchases in India. For instance, this sector grew by a whopping 569% in 2020 and 637% in 2021 to reach an estimated market size of USD 3.7 billion. According to market estimates, the BNPL user base in India is expected to reach 100 million by FY26.

However, the actual costs customers may incur have not been documented in the Indian context. This report by Dvara Research attempts to address this issue in detail. Their analysis presents insights from studying BNPL products of ten different BNPL providers in India and the findings help put a spotlight on customer protection concerns in the BNPL market. They conclude the report as:

The examination suggests that BNPL products can impose high monetary costs that may be comparable to those imposed on credit cards usage – we caveat this by saying that a more thorough examination of actual costs based on customers' usage of BNPL products and credit cards over time is warranted. We were also able to discover significant misalignment between BNPL providers' practices and key conduct obligations towards customers. Such misalignment could impose non-monetary costs, which include loss of creditworthiness, personal data-related harms, and misconduct from providers and their agents.

Dvara Research notes that BNPL providers’ terms and conditions are misaligned with key customer protection practices and thus, violating key conduct obligations. Customers are at risk of:

Unknowingly incurring debt

Borrowing credit that is unsuitable for them

Being subject to aggressive debt collection practices

When it comes to user experiences with using BNPL products, they observe that “the onboarding and purchase experiences of the volunteers were seamless and completely digital. Barring a couple of rejections, all volunteers successfully registered for the BNPL product and made their purchase. However, specific information about the costs of the BNPL product, like interest rate, processing fee and other charges, was not prominently displayed before the onboarding process.”

The report is pretty informative and well-researched. Please check it out here and its summary analysis here and here.

9. Global Financial Watchdog FSB to Propose Crypto Regulations in October

The Financial Stability Board (FSB), an international body that monitors financial systems and proposes rules to prevent financial crises, plans to present recommendations for regulating crypto in October, according to a statement on Monday. This is huge as the Financial Stability Board reports to the Group of 20 of the world's largest economies. The recommendations will cover stablecoins and other crypto assets. They note:

The failure of a market player, in addition to imposing potentially large losses on investors and threatening market confidence arising from the crystallisation of conduct risks, can also quickly transmit risks to other parts of the crypto-asset ecosystem. It may have spill-over effects on important parts of traditional finance such as short-term funding markets.

The FSB plans to submit a report to the G-20 in October on "high-level recommendations for the regulation, supervision and oversight of stablecoins." The proposed rules may include ways to extend existing frameworks to "close gaps" and implement recommended regulations. These recommendations will greatly impact the way major countries approach the regulatory framework of the cryptocurrency world. At this point, we can only wait till they publish the report. I am closely watching the regulatory developments in the crypto industry, I will keep you updated!

10. Podcasts of the Week

1. Is this the End? | Lyn Alden - Bankless

This was one of the finest macro-podcast I have heard in a while. It covers so many things at once such as the current macro environment, historical analogues to the current global economic situation that is loomed by stagflationary fears, energy crisis, limitation to raising interest rates due to high debt levels, competency of central banks, food & fertilizer markets and its relationship to energy, the potential solutions and the importance of mental health during such times.

The pace of this podcast can be overwhelming at some points (like it did to me!) especially if you are not much familiar with the subject but it is advisable to re-listen to the parts which you perceive to be important!

2. The State v Julian Assange with Gabriel Shipton & Stella Moris - What Bitcoin Did

As the title suggests this podcast focuses on the life, work and high-profile legal case of journalist, activist and cryptographer Julian Assange. Gabriel Shipton is a Film Producer & advocate for his brother Julian Assange; Stella Moris is a lawyer & wife to Julian Assange. In this interview, they discuss the unprecedented state assault on Assange’s freedom, the extra-territorial application of US Law, the effects on his mental & physical well-being, & the threat to journalism.

I have read and watched lots of stuff on Julian Assange but I personally felt this interview was heart-touching and I felt the necessity of sharing with you. While you are here, I would also recommend the previous podcast by Peter McCormick (the host of What Bitcoin did), when he interviewed Julian Assange’s father and brother, John and Gabriel Shipton. The podcast dives way deeper into Julian’s case, the importance of Wikileaks, suppression of journalistic freedom and more.

In the end, they also discuss the relationship between Wikileaks and Bitcoin, Satoshi Nakamoto’s pragmatic position on the matter and how they survived the banking blockade with the help of bitcoin donations. Please check it out!

3. The Dangers of Tech that Tracks Everything We Do - Tech Won’t Save Us w/ Shoshana Wodinsky

Paris Marx is joined by Shoshana Wodinsky to discuss how the digital infrastructure that companies have built out over the past couple of decades to track everything we do to serve us ads places us at risk, and how that’s come into focus since the overturning of abortion rights in Roe v Wade in the United States.

4. India Cracks Down on Online Expression - Tech Policy Press

In this podcast, Tech Policy Press focus on the Indian government’s efforts to create a bureaucratic apparatus to enforce what appears to be an ever more frequent number of requests for social media platforms to remove content deemed inappropriate for one reason or another. This podcast discussion touches on a range of issues, including:

The political context and regulatory precedent for the 2021 rules implemented by the Ministry of Electronics and Information Technology and the recently proposed amendments to them.

The dangers of weakening encryption with the goal of allowing.

The challenges and dangers of establishing government bureaucracies to manage social media content moderation and ‘grievances’ that arise.

5. China’s Houses of Cards - Finshots Daily

In this episode, Finshots analyze why Chinese real estate developers are trying to sell property in exchange for wheat, garlic and watermelons.

6. Causes and costs of populism - VoxTalks Economics

Across Europe and beyond, populist movements have recently flourished. What does history teach us about the economic impact of populism – and is our taste for populists a bug or a feature of democracy? Tim Phillips talks to Moritz Schularick and Massimo Morelli.

That’s all for this week folks, and thank you so much for making it this far! I hope you had lots of takeaways. Please subscribe if you haven’t yet and kindly tell your friends to do the same. Subscriptions won't cost you a penny and it is the best way to support my work! If you have any positive feedback, then please do not hesitate to contact me. Thank you :)

Have a great week ahead,

Shreyas