Analyzing the trends of Equity Prices and Equity Risk Premium and their significance

Investing in stock markets is all about taking risks. We all are aware of the fact that taking higher risks lead to higher returns on your stock portfolio. While a risk-averse attitude leads to lower returns on your stock portfolio. In simple words, an equity market is a market in which shares of various companies are issued and traded. It is also known as the stock market and it is one of the most important areas of a market economy.

The importance of Equity Prices

Given the interconnectedness of the market economy, the trends in equity prices are even important to a person who does not invest in stocks and other similar assets. The trends in equity prices reveal expectations of economic agents, reflect the health of the economy and provide useful information to policymakers for shaping their policies to achieve price stability, output stability and economic growth. Thus, equity prices act as a useful input tool for monetary policymaking. It should be noted that the transmission of monetary policy takes place through various financial channels such as financial assets, which ultimately influences the real sector of the economy. The real sector of an economy is the important sector as activities of this sector persuades the total economic output of a country and is represented by those economic agents (households and firms) that are essential for the progress of the economy.

According to the traditional equity valuation model, stock prices are equal to the present value of expected future earnings. Therefore, rising equity prices reflect optimism over the future profitability of companies. The movements in equity prices also help to identify the risks in an economy as it contains information about the degree of uncertainty around the economic outlook. If the market anticipates uncertainty in future and has a high-risk perception, then it is usually associated with low equity prices because investors demand higher premium/reward to compensate for higher risk against alternate safer investments in government bonds thereby driving equity prices even lower.

If this is getting confusing, allow me to explain with an example. In times of uncertainly, say the pandemic or political instability, the expected future earnings of the companies is likely to go down and hence, equity prices are likely to decrease (since equity prices are calculated using the present value of expected future earnings). In such times of uncertainty, a risk-averse investor is likely to invest in risk-free assets like 10-year government bonds that offer 5.9% annually but if an investor is willing to take risks, then he expects much higher returns (>5.9%) than returns offered by risk-free assets.

The evaluation of trends in equity prices and the factors that influence these prices assumes significance from the standpoint of its linkages with the macroeconomy of any country. It directly or indirectly affects the consumption, savings and investment patterns of economic agents. Therefore, the central banks of the country regularly monitor movements in equity prices for achieving their targets of financial stability of the country. An article by RBI on equity prices perfectly puts it:

Central banks also monitor equity prices in pursuit of their objective of maintaining financial stability, which is a prerequisite for price and economic stability. Financial stability risks may arise when equity prices deviate from fundamental levels as dictated by the present value of future income stream and the market is characterised by wide fluctuations in prices. Easy monetary policy for a sustained period may lead to build up of financial excesses by raising equity prices which foster excessive credit risk taking being translated into excessive investments and thereby fuelling asset prices further. These kinds of unsustainable booms not only lead to misallocation of resources but also create systemic risk with serious ramifications for real economy in an event of inevitable market correction, which would warrant appropriate action from monetary policymakers.

What is Equity Risk Premium?

The Reserve Bank of India defines Equity Risk Premium (ERP) as, “ERP is conceptualised as the excess return that makes an investor indifferent between holding a risk-free investment, usually a government bond, and a risky equity investment.” In simple words, an Equity risk premium is an excess return an investor gets for investing in a risky equity asset over a risk-free asset. The formula of Equity Risk Premium is:

Equity Risk Premium: - Market Expected Rate of Return - Risk-Free Rate

It is an indicator of uncertainty and depends upon multiple factors such as investor risk preference, macro-economic fundamentals, savings rate, market liquidity, political stability, government policies and monetary policy. ERP is often interlinked to equity prices and thus warrants the need for monitoring. A more predictable and certain economic scenario in the future provides a viable environment for investment in equity shares and thus it leads to lower risk premium and higher equity prices. Similarly, if the investors are anticipating economic uncertainly in the future then it leads to higher risk premium and lower equity prices.

In this regard, several studies have established the relationship between equity risk premium and various macroeconomic factors. When interest rates decline in an economy, it results in lower rates on risk-free assets. Due to lower rates offered by risk-free assets, investors turn to equity markets for higher returns. Similarly, if inflation rises in the economy then interest rates would go up and as a result of which returns from risk-free assets would also go up. Due to comparatively higher returns, this will incentivize investors to invest in risk-free assets over risky equity assets.

The trends in Equity Risk Premium and Equity Prices

Economists and financial analysts calculate the equity risk premium using various methods such as Capital Asset Pricing Model (CAPM), Dividend Discount Model (DDM) and so on. The methodology that RBI has adopted to calculate equity risk premium is Dividend Discount Model. The DDM approach involves discounting the expected cash flows in the future by using an appropriate discount rate.

The graph depicted above plots equity risk premium over the time period of 2005-2020. The RBI article reveals that the average ERP between 2005-2020 was 4.7%. It can be clearly observed that equity risk premium peaked at 8.2% during the global financial crisis of 2008. ERP started surging again in 2020 as it reached 6.0% in March 2020. The surge in equity risk premium was triggered by the economic uncertainty on account of coronavirus induced stress in the market. Hence, it is safe to conclude that in times of economic uncertainty due to political instability, wars, pandemics and other emergencies - ERP is likely to surge since investors want more compensation for the risk they undertake for investing in risky equity assets.

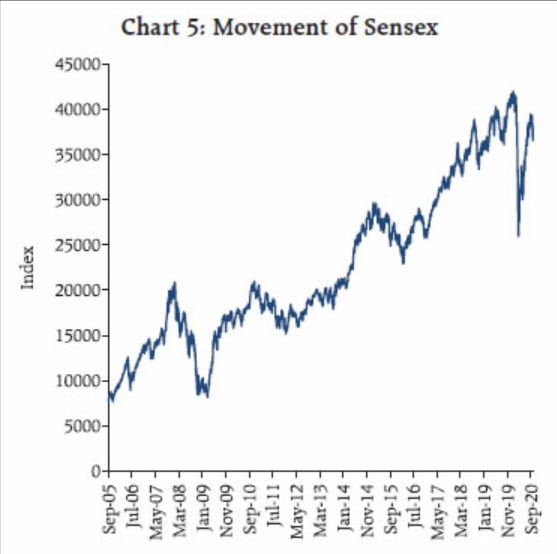

The RBI study also analyses the trend in equity prices over the same time period. It can be observed that in the boom period of 2005-2008, there was a sharp rally in the Indian equity market due to higher expected future earnings. It is obvious that ERP in the boom period of 2005-2008 declined steadily as investors anticipated a viable economic outlook in the future. The boom period was followed by the Global Financial Crisis of 2008 where the Indian equity market declined by over 60% in a short span of 15 months. The future expected earnings declined sharply as the economic outlook worsened due to the financial crisis and as a result, equity risk premium spiked owing to increased perception of risk and uncertainty.

The Indian Equity market witnessed yet another run from February 2016 to January 2020 as the BSE Sensex gained over 80 per cent touching a lifetime high of 41953 on January 14, 2020. The boom was fuelled by not only higher expected future earnings but also by the lower interest rates. It is quite evident from the graph that the equity risk premium remained below average in these years. This “interest rates led” bull run was followed by a sharp correction in the Indian equity market in sync with the global markets due to the COVID-19 pandemic. Equity risk premium in the second phase of 2020 surged as the economic uncertainty loomed the market sentiments due to lower earnings expectation triggered by the pandemic.

In the end, the paper also highlights the disconnect between stock prices and the real economy in reality. The paper states:

The regression results suggest that while the increase in ERP assumes significance in explaining the dependent variables, that is, IIP and GDP (economic activity indicators), decrease in ERP is insignificant in line with the economic theories. This is largely consistent with the divergence between real economy and market observed in 2019 wherein ERP stayed low contributing to surge in equity markets to record-highs and GDP growth stayed muted. Overall, while the ERP has stayed below 4 percent levels since 2016, real GDP growth has remained below 2016 level which was 8.7 per cent.

For further reading, you can access the article released by the RBI here.