The Economics Hub Newsletter: Week 6

India topping remittances, mid-year investment outlook, ECB raising interest rates, rising default risk among EM nations and other article recommendations

Happy Sunday!

Welcome to another issue of The Economics Hub Newsletter! I hope you are well.

If you have already subscribed, thank you! If you are here for the first time, then please consider subscribing for free educational content and resources!

Here’s what we cover this week. As per your interest and convenience, please click on the specific topic to jump directly to that section!

Ready? Let’s dive in!

With $89 billion, India top remittance recipient in 2021: UN report

Bank of America Global Fund Manager Survey Shows Full Investor Capitulation Amid Pessimism

Many Developing Countries are increasingly Vulnerable to the Risk of Sovereign Debt Default

The European Central Bank has raised interest rates for the first time in 11 years

1. Tor Browser now bypasses internet censorship automatically

The Tor Project has just recently released the updated Tor Browser 11.5. It is available on the Tor Browser download page and also on their distribution directory. This new release is noteworthy as it builds upon features introduced in Tor Browser 10.5 to transform the user experience of connecting to Tor from heavily censored regions. For those in countries such as Belarus, China, and Russia where Tor is blocked, the typical way to get around this censorship onto the network is via “Tor bridges.”

However, circumventing censorship of the Tor Network itself remained a manual and confusing process – requiring users to dive into Tor Network settings and figure out for themselves how to apply a bridge to unblock Tor. This manual bridge configuration placed the burden on censored users to figure out what option to pick, resulting in a lot of trial, error and frustration in the process. With this new update, the Tor Project seeks to reduce this burden with the introduction of Connection Assist: a new feature that when required will offer to automatically apply the bridge configuration they think will work best in your location for you.

Check their blog post for more details!

2. With $89 billion, India top remittance recipient in 2021: UN report

India received 89 billion dollars in remittances in 2021, the top remittance recipient, and way ahead of countries like China and Mexico, according to a World Health Organisation report released on Wednesday. The report by the specialised agency of the United Nations responsible for international public health said that in 2021 the top five remittance recipients in current US dollars were India, China, Mexico, the Philippines and Egypt.

The report notes that India gained a substantial 8% during the year, as a return of migrant labour to host countries and support to reduce the effects of COVID-19 in India boosted remittance inflows. Furthermore, recent experience from the pandemic suggests that migrants will continue to send remittances to their families in 2022. There is a possibility that the opening of the region’s economies will offer them the option to send more money through informal and digital than formal traditional money transfer channels, leading to a decline in recorded formal remittance inflow.

In its July 2022 report, the Reserve Bank of India noted that India’s inward remittances have proven to be a resilient source of current account receipts. Furthermore, the cross-country remittances inflows are found to be driven by altruism motive, captured by the infection rate in the destination country and the stringency of the lockdown in the source countries. For instance, overseas remittances for family maintenance represented a huge chunk of India’s inbound remittances, while local withdrawals from non-resident rupee-denominated deposit accounts increased substantially, implying the drawdown of savings to tide through the crisis.

You can read the report for more analysis, details, charts and tables. Please check it out!

3. J.P. Morgan Mid-Year Investment Outlook 2022

J. P. Morgan recently released a mid-year market insights report which summarizes the performance of financial asset classes and presents an outlook for the same. It is a good overview and I think it reflects the mildly increasing confidence of the investment banks in the economic rebound by next year. The summary of the report is presented below:

JPM’s central scenario is that we could avoid a severe global downturn thanks in large part to fiscal support, and a more gradual pace of tightening by the central banks in the second half of the year. With major markets having already experienced double-digit declines, the significant further downside for risk assets is not their base case.

With inflation as the root cause of the problem, investors have found themselves in the worst of all worlds, with the price of both bonds and stocks falling. For instance, fears of stagflation have caused the traditional 60:40 portfolio (conventionally considered as a "balanced portfolio" as 60% is invested in stocks and 40% in bonds) to trade over 18% lower year-to-date. As you can see from the chart below, it rarely happens.

Source: JP Morgan Mid-year Investment Outlook 2022 However, JPM foresees that the risks to government bond prices are now more evenly balanced and bonds can now offer some portfolio diversification in the more extreme negative scenarios.

Signs of cooling economic activity could allow for a more gradualist approach from the central banks. This should limit the downside risk for assets and re-establish the negative correlation between stocks and bonds that had previously proved so helpful to investors trying to construct a balanced portfolio.

Value stocks have outperformed growth stocks significantly this year. The MSCI World Index is down by over 20% but within that, the MSCI World Growth Index shrank by 30% while the MSCI World Value Index declined by just 13%. JPM expects value’s outperformance of growth may continue if economic activity proves resilient to higher commodity prices and interest rates.

Until inflation subsides investors will remain concerned about stagflation. Alternatives such as core infrastructure and real estate, and stocks that offer resilient high dividends, are relatively attractive in this challenging backdrop. When the beta of markets is less supportive and capital gains cannot be relied upon, dividends and coupons become more important. Therefore, financial assets that provide sustainable income should be your priority in this stagflationary market framework.

The report also advises the investors to stay invested in the markets and to look for potential opportunities as short-term challenges like these have always planted the seeds for long-term opportunities. For instance, the oil shock in the 1970s led to a tremendous shift in fuel-efficient automobiles and investment in renewable or nuclear energy sectors. Like in the 1970s, the current energy crisis will turbocharge the energy transition and investors will need to identify the relative winners of this trend.

In the end, they also highlighted the need for humility in economic forecasting by analysts as their projections have direct impacts on the confidence level of consumers and businesses, and subsequently impact monetary policy decisions.

Forecasting economies and markets are never easy. Understanding the post-pandemic economy and unprecedented policy response further complicates the forecasting process. On top of this, our projections depend on the judgments and decisions of a handful of key individuals: Whether the prospect of a long and costly war causes a strategic rethink in Moscow or whether Putin retaliates against the embargo; whether the central banks and politicians do prioritise growth over inflation and other influencing factors. These many variables demand a degree of humility when forecasting the economic outlook.

4. Bank of America Global Fund Manager Survey Shows Full Investor Capitulation Amid Pessimism

On the contrary, the Bank of America’s latest Global Fund Manager Survey does not provide an optimistic forecast on the financial markets in the imminent future. The survey, which included 259 participants with $722 billion under management was conducted between July 8 and July 15. It shows dire levels of pessimism among investors and their increased preference for cash, signalling bearish sentiment in the financial markets. However, from a contrarian perspective, holding too much cash also means that institutional investors are preparing themselves for buying any upside opportunity that may arise in the future.

Global growth and profit expectations sank to an all-time low, while recession expectations were at their highest since the pandemic-fueled slowdown in May 2020, strategists led by Michael Hartnett wrote in the note. Investor allocation to stocks plunged to levels last seen in October 2008 while exposure to cash surged to the highest since 2001, according to the survey. A net 58% of fund managers said they’re taking lower than normal risks, a record that surpassed the survey’s global financial crisis levels.

Bank of America strategists said their custom bull & bear indicator remains “max bearish,” which could be a contrarian signal for a short-term rally. “Second half 2022 fundamentals are poor but sentiment says stocks/credit rally in coming weeks,” strategists wrote.

Other notable findings include:

Among equity regions, investors are most bearish on Eurozone and Japan.

Although optimism is brewing again that inflation could be nearing a peak, fund managers largely believe that economic recession is imminent.

Most crowded trades are long US dollar, long oil and commodities, long ESG assets, long cash and short US Treasuries.

In the past 4 weeks, investors increased their exposure to bonds, staples, utilities, and healthcare, while slashing exposure to equities, Eurozone, materials and banks.

5. Many Developing Countries are increasingly Vulnerable to the Risk of Sovereign Debt Default

We have spoken at length about the looming debt crisis in emerging markets and developing economies (EMDEs) in week 4’s newsletter. Please check that article out for understanding the reasons behind the imminent debt crisis in developing countries and the imperative for impactful global action.

As we have noted earlier, Sri Lanka was the first nation to stop paying its foreign bondholders this year, burdened by unwieldy food and fuel costs that stoked protests and political chaos. For all different reasons, Russia followed Sri Lanka and defaulted on its sovereign default in June 2022, for the first time in 100 years! But Russia and Sri Lanka aren’t alone as many debt-distressed countries are expected to follow the suit.

Bloomberg has developed a Sovereign Debt Vulnerability Index, which ranks the countries with the highest default risk. It’s based on four underlying metrics:

Government bond yields

5-year credit default swap (CDS) spread

Interest expense as a percentage of GDP

Government debt as a percentage of GDP

Assuming you might not be familiar with the concept of a credit default swap (CDS) spread, let’s do a quick recap. Credit default swaps (CDS) are a type of derivative (financial contract) that allows an investor to swap or offset their credit risk with that of another investor. To insure against the risk of default, the lender (say foreign investor) buys a CDS from another investor (third-party) who agrees to reimburse the lender in the case the borrower (emerging/low-income country) defaults. If a CDS has a spread of 300 bps (3%), this means that to insure $100 in debt, the investor must pay $3 per year. As you can see from the following chart by Visual Capitalist, the 5Y CDS spread is pretty high in countries such as El Salvador, Ukraine and Argentina.

The number of emerging markets with sovereign debt that trades at distressed levels — yields more than 10 percentage points above that of similar-maturity Treasuries, which can indicate investors believe the default is a real possibility — has more than doubled in the past six months, according to data compiled from a Bloomberg index. Collectively, those 19 nations are home to more than 900 million people, and some — such as Sri Lanka and Lebanon — are already in default. Collectively, almost a fifth — or about 17% — of the $1.4 trillion emerging-market sovereign bonds are trading at distressed levels.

Historically, debt defaults have shown that it has the potential to trigger political turmoil among the masses resulting in overthrowing governments, food & fuel shortages, the absence of manufacturing and industrial activity, etc. “There’s a lot of academic literature and historical precedence in terms of social instability that higher food prices can cause, and then that can lead to political change”, said Anupam Damani, head of international and emerging-market debt at Nuveen.

Samy Muaddi, a portfolio manager at T. Rowe Price, points out that many emerging markets rushed to sell overseas bonds during the Covid pandemic when spending needs were high and borrowing costs were low. Now that global developed-market central banks tighten financial conditions, driving capital flows away from emerging markets and leaving them with heavy costs, some of them will be at risk.

Continue reading the article by Bloomberg, for a country-wise analysis of debt-distressed nations and the different geopolitical and economic factors that led them here.

6. Off-Topic ChartStorm: Emerging Markets

If you are interested in other interesting technical graphs related to Emerging markets w.r.t. debt levels, bond spreads, currencies, etc. then I would recommend you checking it out this newsletter by Callum Thomas.

Callum’s newsletter presents the following charts w.r.t Emerging markets, Please check it out if any of these topics interest you!

Emerging Markets (EM) vs Developed Markets (DM) Relative Performance in Perspective.

Emerging Markets Country Breadth

EM performance w.r.t US Dollar Index

EM Commodity Currencies Index

JPM EM Global Spread

EM Sovereign Stress

Investors abandoning EM bonds

EM Bond Technicals

Emerging Market equity valuations are close to 2009 lows

"High and Falling Inflation" regimes

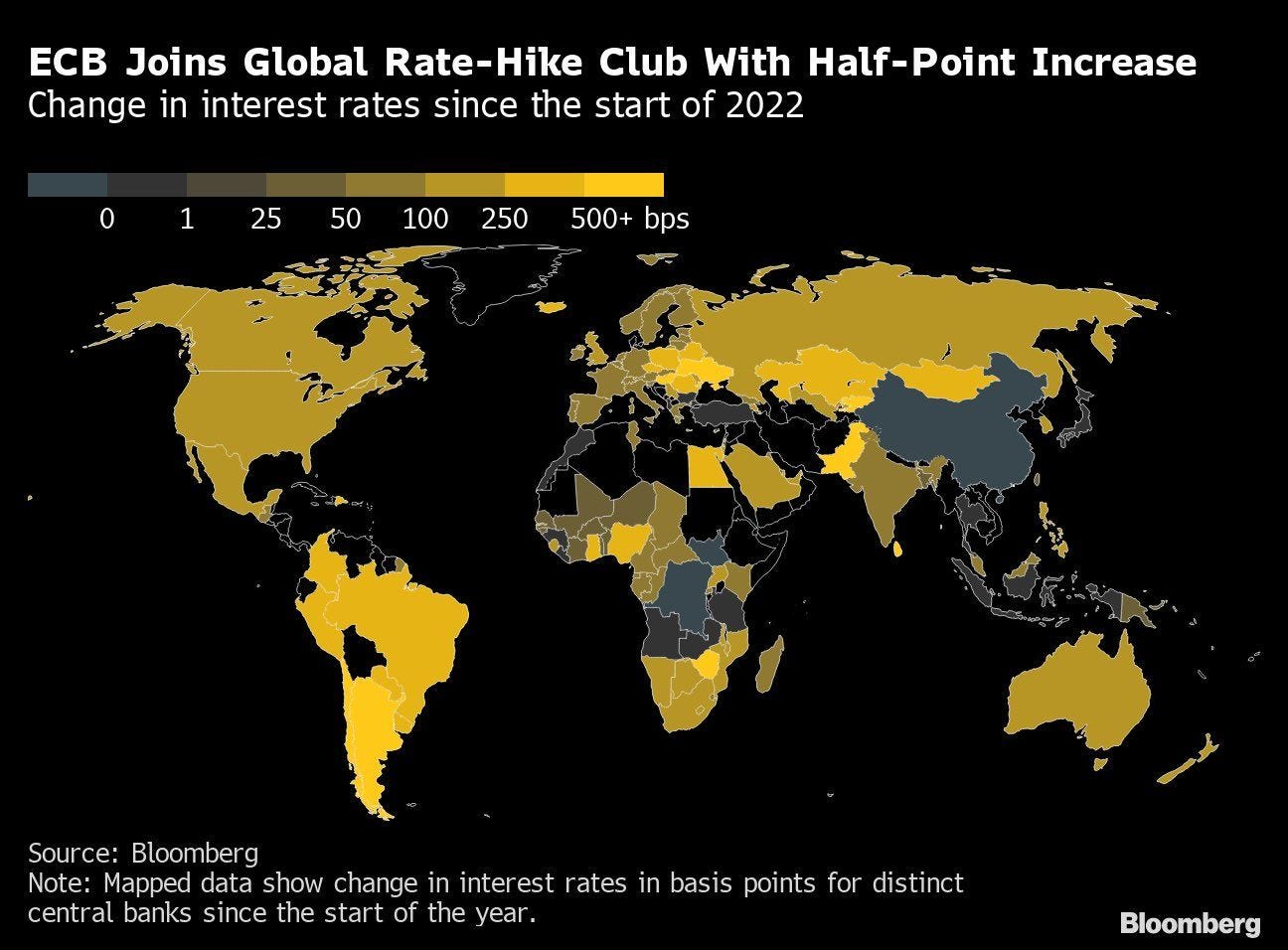

7. The European Central Bank has raised interest rates for the first time in 11 years

In the last week’s newsletter, we discussed the ECB’s policy dilemma in raising interest rates amidst Intra-European bond spreads and ECB’s commitment to mitigate the fragmentation risks associated with it. I would recommend reading that part before proceeding because it is relevant to this topic.

This week, in a bold move the European Central Bank hiked its key interest rates by a half percentage point. That marks the first time since 2011 that the ECB has raised rates, and takes Europe's main rate back to zero. Rates in the region have been negative since 2014. The central bank had previously indicated that it would increase rates by a smaller margin (25 bps), but decided it needed to be more aggressive based on an "updated assessment of inflation risk."

Some of the meeting and press conference headlines can be summarized as follows:

Further normalisation of interest rates will be appropriate, essentially signalling more rate hikes in the coming months.

From now on, decisions will be made “meeting to meeting” in reaction to incoming data. The ECB doesn’t know what the data will be yet, so it can’t guide the rest of us on what its monetary policy will be.

Inflation continues to be undesirably high and is expected to stay above our target for some time.

In the baseline scenario, there is no recession, neither this year nor the near year according to ECB President Christine Lagarde.

Furthermore, they released some details on the new anti-fragmentation tools - policy initiatives aimed at preventing “unwarranted” moves in bond spreads (read my previous week’s newsletter for better understanding) across EU nations. The so-called “Transmission Protection Instrument can be activated to counter unwarranted, disorderly market dynamics that pose a serious threat to the transmission of monetary policy across the euro area," the central bank said. The ECB stands ready to deploy the instrument if necessary, granted that countries meet certain metrics for fiscal and economic health, Lagarde emphasized. You can read more about The Transmission Protection Instrument, ECB’s new anti-fragmentation tool here.

Bloomberg analyst John Authers noted that the investors are still not convinced with ECB can do what is needed to keep Italy in the eurozone. As he describes it:

Under the TPI, the central bank can buy securities “to counter unwarranted, disorderly market dynamics that pose a serious threat to the transmission of monetary policy.” It gives a series of conditions, but no numbers. Any financial interventions will be wholly at the discretion of Lagarde and her colleagues. And to quote Jean Ergas, chief strategist of Tigress Financial Partners in New York, this means that “unwarranted” and “disorderly" could become the new “transitory.” Decisions over intervention will hinge over definitional arguments about those words, adding more confusion to ECB’s actual policy stance.

I tend to believe along the same lines as the ING, who viewed the rate hikes move as:

The hike, as well as potential further hikes, are all aimed at bringing down inflation expectations and to restore the ECB’s damaged reputation and credibility as an inflation fighter. Today’s decision shows that the ECB is more concerned about this credibility than about being predictable. This matters more than forward guidance.

8. Bitcoin and the True Meaning of Inflation

Bitcoin is commonly presented as a hedge against inflation. Since Bitcoin has a fixed supply of 21 million, and fiat is a mind-numbing bacchanalia of printing and excess, it simply makes intuitive sense that Bitcoin would protect people, investors, and portfolios from the ravages of inflation. So why hasn’t it so far in these inflationary times, where the price increase has been observed in commodities, goods and services for over the last 7 months? This article by Steven Lubka presents some compelling arguments which untangle the myth about inflation and bitcoin.

His arguments stem from the core definition of inflation in a historical sense in which inflation was referred to as an increase of paper currency against the supply of fixed collateral (gold, silver) that backed the paper notes. He asserts that Bitcoin can be a great hedge against the debasement of the currency caused by the expansionary monetary policies pursued by the central banks, rather than being a hedge against consumer price increases - which are influenced by multiple factors in the real world. As he brilliantly puts it:

Bitcoin exists to provide users an alternative to irresponsible and fatalistic central bank monetary policy. After all, the headline cited in Bitcoin’s genesis block is “Chancellor on Brink of Second Bailout for Banks, ” not “Supply Chains Face New Obstacles.”

The goal of Bitcoin is clearly something that stands in opposition to central banks and their policy errors. We have to accept that bitcoin will not provide a hedge against CPI increases and that to hedge against central bank actions is to be in a directional relationship with those actions.

Furthermore, Steven argues that it is impractical to expect the “dollar-denominated price” of any financial asset class to be un-impacted in an era where central banks are rapidly withdrawing liquidity from a dollar-centric world. In a recent interview, Macro strategist Lyn Alden also echoed the same conclusions about the relationship between Bitcoin and the broad money supply. As she states:

There are different types of inflation. There’s monetary inflation and then there’s price inflation that often comes with a lag after that monetary inflation, and what we’ve actually seen for the most part is that Bitcoin is correlated very strongly with money supply growth, global M2 especially as measured in dollars, and so over the past couple years as we got that huge ramp up in broad money supply around the world, Bitcoin did very well.

I do understand that arguments like these might not sound convincing to you at the first sight but upon closer inspection of the debt-driven, overly-financialized dollar-centric world and visualizing the end game scenario, this defence of Bitcoin becomes more persuasive from a long-term perspective. If my summary of the article wasn’t enough, you can check out the article and Lyn Alden’s interview for a better understanding!

That’s all for this week folks, and thank you so much for making it this far! I hope you had lots of takeaways. Please subscribe if you haven’t yet and yes, subscriptions won't cost you a penny. It’s free!

Also, please help me spread the word by telling your friends about my newsletter and encouraging them to subscribe. It would mean a lot :)

Have a great week ahead,

Shreyas