The Economics Hub Newsletter: Week 4

Debt Crisis in developing countries, RBI's Financial Stability Report, CBDC update, rising banking frauds, India's new IT rules, and other article recommendations

Happy Saturday!

Welcome to another issue of The Economics Hub Newsletter! I hope you are well.

If you have already subscribed, thank you! If you are here for the first time, then please consider subscribing for free educational content and resources!

Here’s what we cover this week. As per your interest and convenience, please click on the specific topic to jump directly to that section!

Ready? Let’s dive in!

Debt Crisis in Developing Countries: The Imperative of Global Action

Are Indian Equity Markets still Overvalued? Here’s what RBI says

Rise of the Central Bank Digital Currencies: Drivers, Approaches and Technologies - BIS Report

More African Central Banks Are Exploring Digital Currencies (CBDCs)

Banking-Related Frauds are Becoming Prevalent in India. Here’s What You Can Do

Cybersecurity Deals Surge Amid Rising Attacks - Podcast by Goldman Sachs

Payment Failures in Direct Benefit Transfers - Dvara Research Report

Copper price plunges to a 20-month low and historic recession alarm bells are ringing

The End of Roe Will Bring About a Sea Change in the Encryption Debate - Stanford Law School

1. Explainer: The Economic Crisis in Sri Lanka

Sri Lanka is currently in an economic and political crisis of mass proportions, recently culminating in default on its debt payments. The country is also nearly empty on its foreign currency reserves, decreasing the ability to purchase imports and driving up domestic prices for goods.

There are several reasons for this crisis and the economic turmoil has sparked mass protests and violence across the country. The infographic and analysis presented by Visual Capitalist in this article break down some of the elements that led to Sri Lanka’s current situation mainly, high debt levels, depleting forex reserves, currency devaluation, the collapse of the lucrative tourism industry and heavy reliance on imports for their essential needs such as food and energy.

The combination of these factors makes it remarkably harder for the Sri Lankan government to:

Finance their imports using depleting forex reserves, currency depreciation and higher global commodity prices

Borrow fresh money it needs from the international creditors, due to their weak economic outlook and damaging reputation in the money markets as a result of debt defaults.

Some sort of debt structuring or IMF bailout could help but the scarier thing is that what’s happening in Sri Lanka may be an ominous preview of what’s to come in other low and middle-income countries, as the risk of debt distress continues to rise globally.

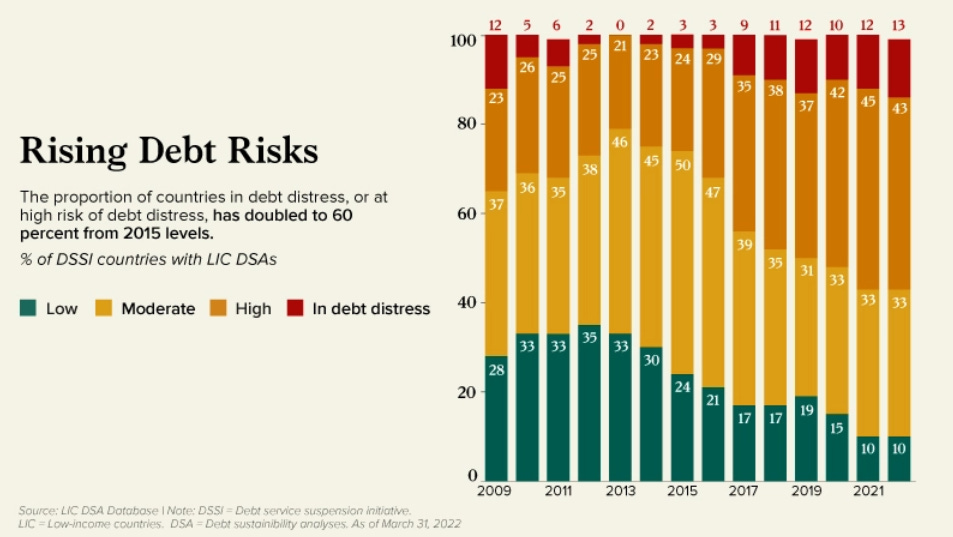

2. Sovereign Debt Sustainability in Developing Economies: The Imperative of Global Action

We just covered how the situation in Sri Lanka has been worrisome - economically, socially and politically. But Sri Lanka is not alone in this distressing situation. There is a debt crisis looming in emerging markets and developing economies (EMDEs) that has the potential to create widespread economic distress for a majority of the world’s population. IMF managing director Kristalina Georgieva stated that 60% of low-income countries are “at or near debt distress” and at least 20 African countries fall into this category. The inability of these cash-strapped countries to service their debts without any international assistance makes them vulnerable to economic distress followed by social unrest and political instability.

But how did we get here? Well, there are several factors but the debt levels were already surging in developing economies during pre-covid times. United Nations Conference on Trade and Development reported that the total debt service on external debt in the least developed countries rose from $33 billion in 2019 to $50 billion in 2021—each figure is a far cry from $10 billion in 2013. Coronavirus and the economic turmoil that followed exacerbated the situation even further as it limited their ability to raise resources domestically. Other key factors are:

Supply chain disruptions caused by Covid-19 haven’t completely waned so far.

War in Ukraine has led to an increase in global food, energy and fertilizer prices.

Monetary tightening led by major central banks around the globe has resulted in foreign investors pulling off their capital from developing countries as they find refuge in dollar-denominated financial assets - putting more pressure on their domestic currencies.

Credit rating agencies (CRAs) downgrading the outlook for many developing and low-income economies due to their high debt levels and the increasing possibility of debt defaults in the imminent future, making it harder for these countries to gain access to new sources of financing. Remember, credit rating agencies provide information to investors, institutions and financial markets to help them price risk, and thus can directly impact the foreign investments and the inflow of foreign capital in these countries. Historically, negative warning announcements by CRAs have been linked to increases in the cost of borrowing for low-income and developing countries. Credit ratings can essentially augment market volatility.

This article provides some key measures to manage the worsening debt profiles of these countries. These are:

The first is to urge the international community to use some of the measures adopted during COVID-19 to help manage the situation (temporarily).

Making a case for international cooperation via a comprehensive framework for managing debt that would accommodate the more expensive debts owed to commercial creditors as well as debts to other big lenders.

Re-thinking of the international financial architecture for addressing both the lack of adequate access to development finance and the challenges posed by precarious debt sustainability.

3. RBI releases the Financial Stability Report

On June 30th 2022, the Reserve Bank of India released the 25th issue of the Financial Stability Report (FSR), which reflects the collective assessment of the Sub-Committee of the Financial Stability and Development Council (FSDC) on risks to financial stability and the resilience of the financial system. It is published bi-annually and includes contributions from all the financial sector regulators. Some key highlights:

The outlook for the global economy is shrouded by considerable uncertainty on account of the war in Ukraine, elevated commodity prices, supply chain disruptions and darkening growth prospects. In tandem, front-loaded monetary policy normalisation in response to persistently high inflation is imparting high volatility to global financial markets. The evolving outlook is particularly challenging for emerging market economies (EMEs) that face rising indebtedness, currency depreciations, capital outflows and reserve losses, even as they grapple with the ravages of the pandemic.

Banks, as well as non-banking financial institutions, have sufficient capital buffers to withstand shocks. “Macro-stress tests for credit risk reveal that Scheduled commercial banks (SCBs) are well-capitalised and all banks would be able to comply with the minimum capital requirements even under adverse stress scenarios.”

Strengthening the regulation of non-bank financial intermediation remains a priority. Domestically, efforts continue to fortify the financial system against sudden shocks and to improve the credit environment to support the recovery while ensuring macroeconomic and financial stability.

The report points out that the financial stability risks to the Indian economy are skewed towards external factors more than domestic ones. However, the spillover of the external risks to the financial sector stability can be quick in a volatile environment.

Domestic macroeconomic, institutional and general risks were perceived as ‘medium’. Nearly eighty per cent of the respondents judged that the prospects of the Indian banking sector are likely to improve or remain unchanged over a one-year horizon.

The report is richly occupied with important statistics, charts, and tables associated with the Indian financial sector. This report is a must-read for anyone associated with the financial sector but I would also strongly encourage you to have a look even if you are from other disciplines.

4. Despite the fall, are Indian stock markets still overvalued?

Just a while ago, we covered the RBI’s latest Financial Stability Report (FSR). It is the main document to understand the current status of risks to the stability of the Indian financial system.

This weekly newsletter by Udit Misra specifically focuses on the status of India’s equity markets and how RBI’s Financial Stability Report perceives it. Some points:

In the last FSR, one of the key observations that caught everyone’s attention was the growing disconnect between India’s stock markets and the real economy.

Over the past few weeks and months, much like several global stock markets, Indian stock markets have come off their all-time highs.

The third reason to look at this issue is driven by the remarkable change in the investor profile of the Indian stock markets since the start of the pandemic. The RBI’s report asserts that domestic investors still support Indian equity markets despite foreign investors having pulled off their capital from the market in recent months, leading to the capping of overall losses. In other words, in case the markets are still overvalued, what is at stake is the interest of the domestic investors.

Individual investors’ participation in stock exchanges has increased significantly since the onset of the Covid-19 pandemic and the registration of new investors on exchanges is reaching beyond metropolitan centres and big cities. The key reasons for it are a decline in real returns on fixed-income investments, simplification of KYC processes, more awareness and availability of information, and effective use of digital technology.

The RBI’s report then provides 4 key metrics to assess the valuation of Indian equity markets. These are:

The 12-month “trailing” price-to-earnings ratio

The 12-month “forward” price-to-earnings ratio

The market capitalisation to GDP ratio

The Bond Equity Earnings Yield Ratio (or BEER)

You can read the article for a detailed explanation but these metrics signal that the Indian markets are overvalued at the moment. However, a high valuation doesn’t necessarily guarantee a fall in stock markets, just as a low valuation doesn’t imply an immediate surge. But these metrics do help investors become aware of the risks and opportunities.

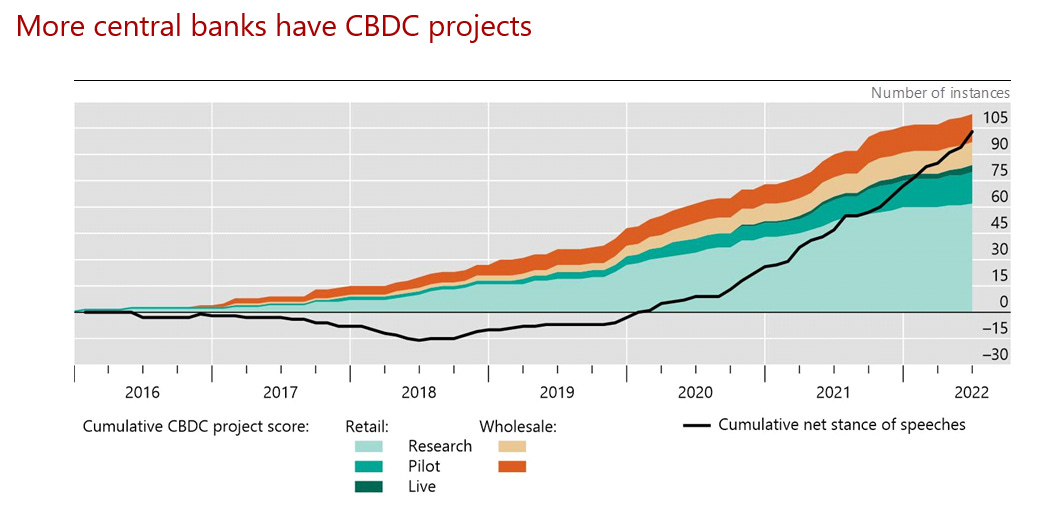

5. Rise of the central bank digital currencies: drivers, approaches and technologies

Central bank digital currencies (CBDCs) are receiving more attention than ever before. However, the motivations for issuance vary across countries, as do the policy approaches and technical designs. In this paper, the Bank for International Settlements (BIS) investigate the economic and institutional drivers of CBDC

development and take stock of design efforts around the world.

Some key findings from the report are:

The drivers of CBDC development and projects originate in digitized and innovative economies.

Retail CBDC work is more advanced where the informal economy is larger. None of the projects surveyed seeks to replace cash - all aim to offer a digital complement.

On the technical designs, the BIS notice that more and more central banks are considering "Hybrid" or "Intermediated" architectures, where the CBDC is a cash-like direct claim on the central bank but the private sector manages all customer-facing activity.

Only a few jurisdictions are considering "Direct" designs, in which the central bank takes on some or all of the customer-facing side of payments. At present, no central bank reports that it is pursuing a "Synthetic" or "Indirect" CBDC design.

While many central banks are considering multiple technological options

simultaneously, current proofs-of-concept tend to be based on distributed ledger technology (DLT) rather than conventional technological infrastructure.The notable highlight of the report is that the access frameworks of CBDCS would be based on account identification rather than allowing for token-based fully anonymous access. Privacy advocates might not welcome this pace of development in the CBDC space.

The mentioned report is from late 2020, but as per their July 2022 update, we can understand the stance of many central banks w.r.t. CBDC design, policy approach and issuance have not really changed much. In fact, central banks are being increasingly involved in the CBDC research and pilot projects.

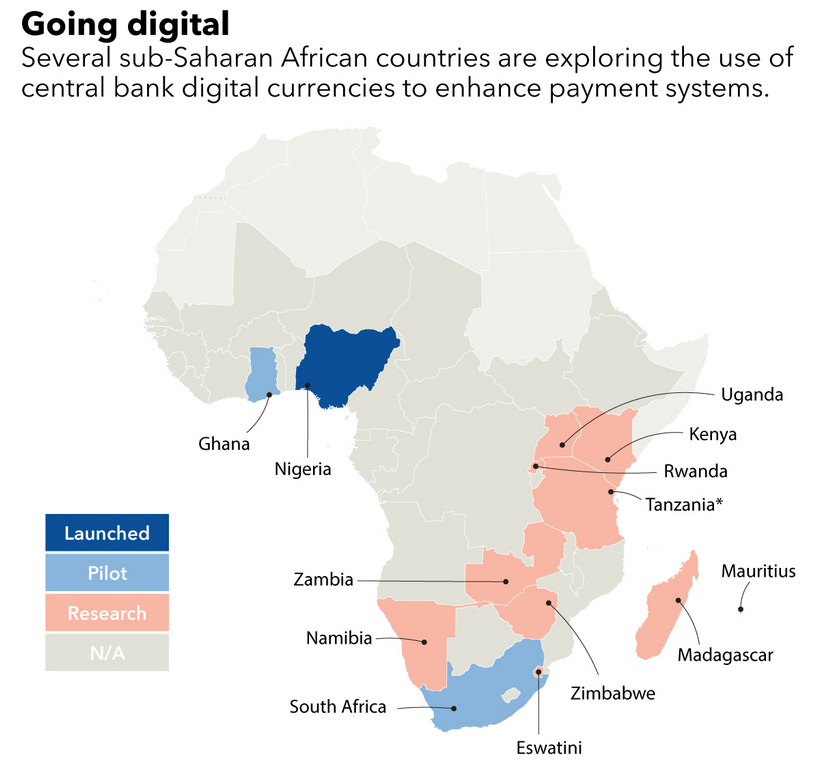

6. More African Central Banks Are Exploring Digital Currencies (CBDCs)

Several sub-Saharan African central banks are exploring or in the pilot phase of a digital currency, following Nigeria’s October introduction of the e-Naira. Nigeria was the second country after the Bahamas to roll out a CBDC.

As you can see from the chart, South Africa and Ghana are running pilots while other countries are in the research phase. Countries have different motives for issuing CBDCs but the IMF observes that the region has some potential benefits from issuing CBDCs. These are:

Promoting financial inclusion. CBDCs could bring financial services to people who previously didn’t have bank accounts, especially if designed for offline use.

CBDCs can be used to distribute targeted welfare payments, especially during sudden crises such as a pandemic or natural disaster.

They can also facilitate cross-border transfers and payments. CBDCs could make sending remittances easier, faster, and cheaper by shortening payment chains and creating more competition among service providers. Remember, Sub-Saharan Africa is the most expensive region to send and receive money.

Thankfully, the IMF blog also discusses the risks and challenges that need to be considered before issuing a CBDC. These challenges are crucial because we all know how the promises of identifying beneficiaries and pushing digital payments for welfare schemes end up in India. Nevertheless, that’s the topic for another day but if you are curious then you can read my analysis of CBDCs here.

7. Banking-Related Frauds are Becoming Prevalent in India. Here’s how to keep your money safe

Banking in India has seen tremendous growth over the last few years, right from instant payments, and money transfers to instant loan approvals. Along with this ease of banking, there has been a side-by-side increase in frauds and the types of frauds. You might be aware of these financial frauds/scams, but I am stating it anyway:

Frauds through WhatsApp/Facebook account: So basically, scammers access a customer's Facebook or WhatsApp account and send messages requesting money to the contacts on the customer's contact list. Usually, your acquaintance ends up sending money to the scammer assuming that they are sending it to you. So the next time you receive a shady message from your friend asking for money, then the bare minimum you should do is by confirming via call or meeting them in person.

Phishing: To obtain customer information like account numbers, login IDs, passwords, mobile numbers, addresses, debit card grid values, credit card numbers, CVV numbers, PAN, dates of birth, mothers' maiden names, passport numbers, etc., scammers use a combination of email phishing, voice phishing, and SMS phishing. They use cutting-edge social engineering techniques to trick users of online banking.

Vishing: Vishing - or voice phishing – is a form of cyber attack that attempts to trick victims into giving up sensitive information like credit card numbers, bank account details and passwords, over the phone. Fraudsters call consumers and pose as bank representatives to deceive them into giving their personal and financial information.

Smishing: Smishing is a phishing cybersecurity attack carried out over mobile text messaging, also known as SMS phishing. Victims are deceived into giving sensitive information to a disguised attacker. SMS phishing can be assisted by malware or fraud websites. Yep, all these shady website links you get over your text could potentially be a smishing trap. Scammers encourage you to open a URL link within the text message, where they then are led to a phishing tool prompting them to disclose their private information.

Kaspersky, an international cybersecurity provider has an informative guide on Smishing and what measures you can take that will help you protect yourself against these scams, frauds and attacks. Similarly, they have explainers on protecting yourself from potential Vishing and Phishing attacks. Check it out!

8. India’s IT Rules & New Amendments: ‘A Threat to Freedom of Expression’

In May 2021, the Indian government codified Information Technology (Intermediary Guidelines and Digital Media Ethics Code) Rules, 2021 - aiming to regulate (control?) social media firms such as Twitter, Facebook, etc. The rules primarily deal with the due diligence duties of “social media intermediaries (SSMIs)”, which are platforms with more than 5 million users (such as Facebook, Twitter, Telegram etc.). SSMIs are also mandated to appoint a Chief Compliance Officer, Resident Grievance Officer, and Nodal Contact person who shall collectively be responsible for ensuring compliance with the IT Act and rules.

Furthermore, they were also instructed to enable the identification of the first originator of the information on its computer resource. WhatsApp has previously said that it can’t comply with such traceability requests without compromising “end-to-end encryption” security for every user. These social media intermediaries were also mandated to inform users at least once every year, in case of non-compliance with rules and regulations. They now have the right to terminate the access or usage rights of the users to the computer resource immediately or remove it in case of non-compliance.

Now, a year later, the Ministry of Electronics and Information Technology (MeitY) proposed amendments to the rules because it feels that the directions were not being complied with properly by a few SSMIs. It also said that there have been numerous instances where intermediaries did not address the grievances “satisfactorily and/or fairly”. The newly issued draft is even more dystopian as it proposes the creation of government-appointed appeal committees that will be empowered to review and possibly reverse content moderation decisions taken by social media companies like Facebook, Twitter and YouTube. The draft proposal has triggered concerns about the government overriding social media platforms’ content decisions.

Simultaneously, SSMIs operating in India have increasingly approved a wave of content removals and account withholding notices for journalists and civil society groups. For instance, on June 27, British Pakistani journalist Murtaza Ali Shah, a reporter at GEO News and The News International, received a notice of his account being withheld in India under local laws. Prateek Waghre of the Internet Freedom Foundation has been maintaining a compiled list of incidents where law enforcement agencies have taken action based on content posted on social media. Please check it out!

“Provisions like these increase costs for companies that may seek to push back against unjust censorship demands, forcing companies to put their staff on the line to protect free speech is a tactic that governments increasingly use to tighten their grasp over the online expression,” said Kian Vesteinsson, a research analyst for technology and democracy at Freedom House.

Delhi-based digital rights organization Internet Freedom Foundation have comprehensively highlighted the illegalities of the proposal and also provided some useful recommendations. These are:

Withdraw IT Rules, 2021 in their entirety.

Revive the erstwhile Cyber Regulations Advisory Committee (“CRAC”) under Section 88 of the IT Act, 2000 with the membership of the civil society, technologists and digital rights experts.

Publish a white paper detailing the government’s intent concerning intermediary liability and online content regulation.

Removing any definitional vagueness to prevent misuse.

Ensuring that any decision to remove content is taken by an independent authority.

Providing procedural safeguards when content is removed such as an obligation to provide reasoned order, a right to be heard to the content creator and the right to appeal the decision of the authority.

Creating a minimum requirement for any forthcoming regulatory framework, so that such provisions provide a basic level of operational transparency.

9. Podcast: Cybersecurity Deals Surge Amid Rising Attacks

The scale and sophistication of cyber-attacks are rising exponentially. But so are the levels of investment, innovation and corporate activity in the space. In the latest episode of Exchanges at Goldman Sachs, David Campbell, managing director in growth equity in Goldman Sachs Asset Management, and Marco Poletti, Goldman Sachs’ head of Cybersecurity Investment Banking, discuss the evolution of technology and the acceleration of investment and M&A activity within the space.

“There was over $30 billion invested in cybersecurity companies last year, so it is a very well-funded space,” Campbell tells Exchanges host Allison Nathan. “The challenge is there are literally thousands of businesses out there. The way we approach it is we're looking for things that have some longevity because typically valuations are quite high even in very early stages of these businesses.”

You can go through the podcast’s transcript if you prefer that way!

10. Payment Failures in Direct Benefit Transfers - Dvara Research

This week we have an excellent blog post by Dvara Research highlighting payment failures during the back-end processing of Direct Benefit Transfer (DBT) payments to welfare beneficiaries. Cash transfers to citizens through the Direct Benefit Transfer (DBT) infrastructure are among the most prominent developments in India’s social protection policy landscape. Their fieldwork and empirical analysis have revealed that such payment failures are leading to the exclusion of many citizens. They have identified various barriers to accessing social protection across four stages of the delivery chain: identification, targeting, payment processing, and cash withdrawal. Few headline findings from their survey:

72.85% of surveyed respondents reported experiencing some issues during the processing of their payments.

18% experienced ‘Bank Account and Aadhaar-related issues, indicating that citizens’ payments failed due to errors in their Aadhaar IDs, KYC procedures, or Aadhaar-bank account seeding.

They provide some recommendations in their report as well:

Improving coordination between organisations involved in the backend processing of DBT payments and beneficiaries’ banks.

They recommend creating a common Grievance Redress Cell for all DBT schemes across tiers: State, District and Block.

Facilitating transparency by improving channels of communication.

For a comprehensive analysis, please read the complete article and their well-researched report titled, “State of Exclusion.”

11. Copper price plunges to a 20-month low and historic recession alarm bells are ringing

Copper prices have fallen to their lowest level in nearly two years, as aggressive interest rates, a spike in covid-19 cases in China, potential recession, and rising inventories weighed on investor sentiment. It is the biggest quarterly percentage decline in more than a decade and trades at its lowest level since November 2020.

Okay, but why this is important and concerning? Well, copper or famously known as Dr Copper, is seen as an economic bellwether because the metal is used in many industrial applications in the real economy including construction, household appliances, and electric vehicles. Falling prices may indicate a sour outlook as fears mount over a global economic slowdown. This industrial metal is particularly sensitive to short-term economic expectations for the industrial outlook and is widely used as a gauge of economic health. This has been a reliable indicator of a looming recession going back as far as the past 30 years.

Other base metals have witnessed a substantial decline as well. For instance, The London Metal Exchange Index, which focuses on aluminium, copper, nickel, zinc, tin and lead, and the S&P GSCI Industrial Metals Index wrapped up the second quarter with the largest percentage declines since 2008.

Furthermore, the disruption in the energy markets due to the Ukraine war has “reprioritized matters,” away from a focus on copper’s role in greener technologies and climate commitment, as policymakers scramble to have energy needs met, says Bernard Drury, president and CEO of hedge fund and alternative investment firm Drury Capital.

Goldman Sachs in their April 2021 report referred to copper as the “new oil” and its role in achieving the Paris climate goals “cannot be overstated.” Therefore, copper’s outlook in the long term is bullish, but in the short term, its dwindling prices ring the alarming bells of economic recession.

12. The End of Roe Will Bring About a Sea Change in the Encryption Debate - Stanford Law School

On June 24, the Supreme Court of the United States overturned Roe v. Wade in a 6-3 vote, unequivocally eliminating the constitutional right to abortion in the country and sending the decision to state legislatures. This blog post by Riana Pfefferkorn is pretty illuminating as it highlights similarities between encryption and abortion. They both save lives. They both support human dignity.

The loss of Roe will unavoidably usher in a new phase of the encryption debate in the U.S., because Roe has been the law of the land throughout the entire time that strong encryption has been generally available. Roe was decided in 1973, and the landmark Diffie/Hellman paper “New Directions in Cryptography” didn’t come out until 1976. In the decades since, strong encryption went from a niche concern of the military and banks to being in widespread use by average consumers – while, simultaneously, the constitutional right to abortion was slowly and systematically chipped away. Nevertheless, Roe still stood. In all the years since 1976, encryption policy discussions about “balancing” privacy rights and criminal enforcement have never had to seriously grapple with what it means for abortion to be a crime rather than a right. That’s about to change.

Riana specifically questions the legitimacy of mainstream encryption advocates from the US, appealing to law enforcement’s interests and settling for middle-ground solutions that do not do much better for human rights, digital rights, etc. She describes the wickedness of law enforcement bodies when it comes to encryption debates as:

The only reason there’s still any “debate” over encryption is because law enforcement refuses to let it drop. For over a quarter of a century, they’ve constantly insisted on the primacy of their interests. They demand to be centered in every discussion about encryption. They frame encryption as a danger to public safety and position themselves as having a monopoly on protecting public safety. They’ve insisted that all other considerations – cybersecurity, privacy, free expression, personal safety – must be made subordinate to their priorities. They expect everyone else to make trade-offs in the name of their interests but refuse to make trade-offs themselves.

That’s all for this week folks, and thank you so much for making it this far! I hope you had lots of takeaways. Please subscribe if you haven’t yet and kindly tell your friends to do the same. Subscriptions won't cost you a penny and it is the best way to support my work! Thank you :)

Have a great week ahead,

Shreyas

A structured newsletter, culminating all the important headlines around the globe and deciphering it into easiest possible way to comprehend. Keep up the great work.

Thanks so much, this is really informative. I'm from the legal field, so I would recommend talking to legal practitioners on reddit or others on how to prevent bank frauds. Eg., These days they send you an SMS with free hotstar link and then they have you fill up your pan card details. Anyway, thanks for the newsletter